A recent report by the Rainforest Foundation UK describes the potential scaling up of the International Finance Corporation’s Forest Bonds programme as “One of the most worrying evolutions of GCF activities in the Congo Basin”.

In 2016, the GCF approved the International Finance Corporation (IFC) as an “accredited implementing agency with intermediary functions”. The IFC thus became an organisation that can finance projects using GCF funding.

Two years later, the GCF shortlisted an IFC concept note for a Multi-Country Forests Bond Programme. On its website the GCF describes this proposal as follows:

A global forests bond programme for REDD+ activities. The Multi-Country Forest Bonds (MFBs) program will mobilize climate finance to avoid deforestation in multiple forest basins by leveraging the investment potential from capital markets. Funding REDD+ activities and providing price support for carbon credits will demonstrate a results-based financing model.

IFC and “forest bonds”

IFC launched its forest bond programme in 2016 when it bailed out the financially struggling REDD+ Kasigau Corridor Programme in Kenya. IFC has been far from transparent about this “forest bond” project. When REDD-Monitor asked IFC a series of questions about its support for the Kasigau Corridor project, IFC’s response failed to answer any of the questions.

IFC’s US$72 million forest bonds proposal to the GCF would expand IFC’s forest bonds programme to private sector REDD projects in the Democratic Republic of Congo, Madagascar, and Peru. The programme was to be presented to the GCF Board at its 23rd meeting in July 2019, but IFC failed to submit an environmental and social assessment in time. GCF’s next board meeting is in October 2019.

Under the proposal, IFC would provide loans to climate initiatives by issuing co-called “forest bonds”. Any company, or private investor, can buy these bonds. Although the bonds are called “forest bonds”, the money does not have to be invested in forest projects, or forest conservation. It can finance any climate initiative, chosen by the IFC.

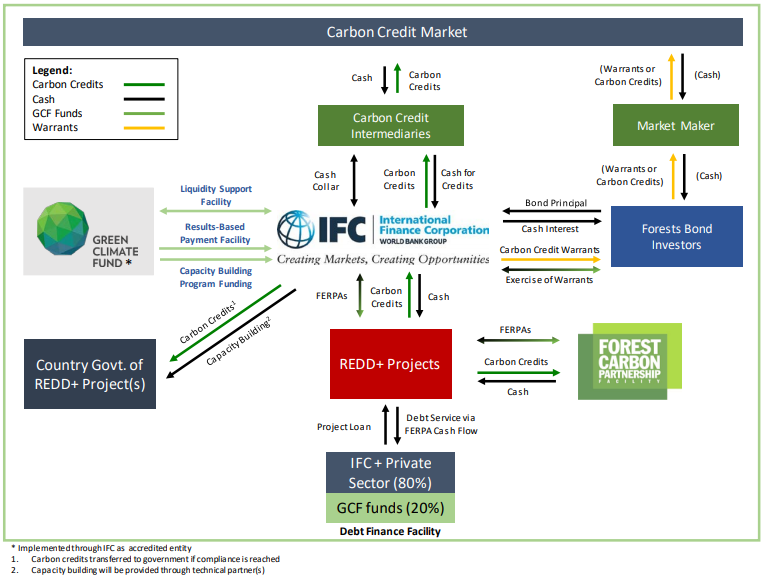

In a June 2018 presentation to the World Bank’s Forest Carbon Partnership Facility, the IFC illustrated the structure of the forest bonds programme with this diagram:

Project developers will make annual interest payments on the loans to the IFC. Bond holders can receive the interest on their bonds in cash, carbon credits, or a mixture of both.

The US$72 million would be divided three ways:

- A Debt Finance Facility (US$12 million): to provide upfront debt financing to private sector REDD projects;

- A Liquidity Support Facility (US$52.5 million): to keep the price of emissions reductions at a minimum of US$5 per ton of carbon – even if the REDD credits are offered to bond holders at less than US$5;

- Capacity Building (US$7.5 million): to integrate private sector REDD projects into jurisdictional REDD programmes.

This is quantitative easing for REDD carbon credits. IFC’s forest bonds programme involves buying near-worthless, probably illegitimate, carbon credits, which have failed for over a decade to raise money for forest conservation. Carbon credits do not address climate change, because for each ton of carbon emissions avoided, the sale of the carbon credits allows climate pollution to continue elsewhere.

IFC will sell its “forest bonds” under a AAA-rating. The IFC, through its financial alchemy, is turning sub-prime carbon credits into a safe investment in forest bonds for the private sector, thanks to massive government subsidies.

RFUK’s report highlights five reasons why IFC’s forest bonds proposal to the GCF is problematic:

- Focus on the international private sector

The benefits of IFC’s Multi-Country Forests Bond Programme are aimed at the international private-sector actors, rather than local communities and countries where REDD projects take place.

The World Bank’s website on the IFC explains that IFC “focuses exclusively on the private sector in developing countries”.

The benefits from IFC’s programme in the Democratic Republic of Congo, for example, will go to the private sector companies running REDD projects there: Wildlife Works Carbon, Somicongo, and Novacel.

It is not clear whether any payments through IFC’s proposal would be additional to payments made under the Forest Carbon Partnership Facility’s US$55 million Mai Ndombe Emissions Reduction Purchase Agreement.

The FCPF was launched in 2007 by the World Bank, with the aim of jump starting a forest carbon market. More than a decade later, the IFC’s forest bond programme is aimed at bailing out a failed carbon market.

Norah Berk, who co-authored RFUK’s recent report, comments that,

“The IFC proposal is devoid of any detail on how it will improve the livelihoods of local communities inside REDD+ areas, and is instead dedicated to propping up a system whose main outcome is likely to only bring financial benefits to international private sector REDD+ actors.”

- The risk of double counting

RFUK writes that there is a “high risk that emissions reductions under the Multi-Country Forests Bond Programme will be double-counted”. Private sector REDD developers could sell REDD credits while the same emission reduction remains in the national carbon account of the host country.

In theory, carbon credits can only be traded if they have not been “cashed in”, or “retired” in a carbon database. But there is no obligation for private sector REDD projects to record all their carbon credits sales in publicly accessible databases.

“There is as yet no proven way of reliably tracking the carbon credits and ensuring that there are not multiple credits with the same tracking number,” RFUK writes.

Emissions reductions can be sold multiple times without being retired thus generating repeated profits for the private sector while communities receive, at best, one single payment.

- An untested market for emissions reductions

The Multi-Country Forests Bond Programme is based on a still untested market for emissions reductions. When IFC launched its green bonds bailout of the Kasigau REDD project in Kenya, it gave investors the option of receiving carbon credits at a fixed price of US$5.00. If investors prefered cash BHP Billiton, the world’s largest mining company (and one of its most destructive), agreed to buy the carbon credits.

So far, none of the investors in IFC’s green bonds have decided to receive their annual interest payments in carbon credits rather than cash.

In the Multi-Country Forests Bond Programme, US$52.5 million of GCF’s funding will go to the Liquidity Support Facility to subsidise what RFUK describe as “unwanted and likely illegitimate carbon credits”.

In other words, almost 75% of GCF’s funding for the green bonds programme is dedicated to removing risk for the IFC (or an intermediary) when selling carbon credits for less than they paid for them.

Joe Eisen, co-author of the report and Head of Research and Policy at RFUK, says,

“The proposal appears to show that the IFC wants a forest carbon market at any cost, even if it shows little sign of actually saving forests. By breathing new life into this ill-conceived and unproven model, the forest bonds programme risks entrenching failures from more than a decade of REDD+ and could serve as a dangerous distraction from the real business of tackling climate change.”

- The private sector and GCF safeguards

GCF’s indigenous peoples policy states that all projects and programmes must obtain the free, prior and informed consent of local communities.

But the World Bank’s Forest Carbon Partnership Facility only requires free, prior and informed consent for projects approved after the Bank’s Environmental and Social Framework was completed in October 2018.

As a result, private sector project developers in the FCPF’s Mai Ndombe programme in the Democratic Republic of Congo only have to obtain “broad community support” through free, prior and informed consultation.

Indigenous Peoples have outright rejected this wording.

RFUK notes that this difference in safeguards remains unresolved:

It is unclear how the GCF intends to reconcile these kinds of discrepancies between safeguard requirements and whether this would disqualify private REDD+ projects from selling carbon credits under the IFC Multi-Country Forests Bonds Programme.

- Do REDD credits represent genuine reductions in emissions?

The Kasigau Corridor REDD project in Kenya is the only project linked to IFC’s forest bonds. RFUK writes that “according to numerous reports”, the project has “not actually led to a reduction in carbon emissions”.

The project’s deforestation reference level was inflated, by basing it on an unrepresentative reference area. The avoided deforestation was thus exaggerated, and the project over-issued carbon credits.

To make matters worse, the project has exacerbated historic inequalities, imposing the harshest restrictions on the most marginalised members of the community.

RFUK comments that,

If the Kasigau Corridor REDD+ project is the exemplary model for selling forest bonds to fund REDD+ programmes, it is likely that funds from the Multi-Country Forests Bond programme in the DRC, as well as other countries, will neither lead to substantial carbon savings nor greatly improved livelihoods of local communities.

This post is the second based on Rainforest Foundation UK’s report, “Good Money After Bad: Risks and Opportunities for the Green Climate Fund in the Congo Basin Rainforests”. REDD-Monitor’s first post based on RFUK’s report is available here.